High-Risk Payment Gateways, eMerchant Authority, is a highly secure platform for businesses that process millions of transactions per year (also known as PCI DSS Level 1). While there are many options for payment gateway providers, we can assure you that none of them will offer you all the tools that eMerchant Authority can provide.

Table of Contents

What is a Payment Gateway?

A payment gateway is an interface between your online store and the payment processor that, as the name suggests, processes the buyer’s credit card. The payment gateway processes the data of the credit or debit card. It authorises or not the payment, making sure that the encrypted data of the card is correct, that there are funds in it, and that the process carries out correctly. Safe. However, payment gateways cannot determine if a card has been stolen or cloned and therefore are not responsible for refund requests.

Why use a High-Risk Payment Gateway?

We have asked ourselves why we use high-risk payment gateways? The reason is straightforward: numerous prestigious offshore virtual POS processors, such as PayPal, Skrill, Xoom, and Safe Card.

They do not want to take the risk of the business that many companies have online since they think the rate of fraud is too high and they don’t earn enough money.

They prefer businesses that have no risk and have to process little money but many transactions; the policies of these companies always benefit the buyer and never the seller. To put an end to this practice, we work with the best high-risk payment processors in the world.

Key Features of a High-Risk Payment Gateway

- High Approval Rates

High-risk businesses (e.g., CBD, gaming, adult, forex, supplements) often face declines with traditional processors. A high-risk gateway is optimized with specialized acquiring banks and smart routing to maximize transaction approval rates.

- Multi-Currency & Global Processing

Supports multiple currencies and international cards, allowing businesses to sell globally without friction. This often includes:

- Dynamic currency conversion

- Local acquiring options

- Cross-border payment optimization

- Advanced Fraud Protection

High-risk industries are more prone to fraud and chargebacks. These gateways include:

- AI-powered fraud detection

- 3D Secure (2.0) authentication

- Velocity checks

- IP and device fingerprinting

- Chargeback Management Tools

Built-in tools help monitor, prevent, and respond to disputes:

- Real-time chargeback alerts

- Automated representment systems

- Chargeback ratio monitoring dashboards

- Multiple Payment Methods

Supports a wide range of payment options:

- Credit & debit cards

- Digital wallets (Apple Pay, Google Pay)

- Alternative payment methods (APMs)

- Bank transfers and ACH

- Recurring Billing & Subscription Management

Essential for industries like SaaS, streaming, and membership platforms:

- Automated recurring billing

- Smart retry logic (dunning management)

- Flexible billing cycles

- Payment Routing & Redundancy

If one acquiring bank declines a transaction, the system can automatically reroute it to another processor — reducing lost sales and downtime.

- Rolling Reserves & Risk Mitigation Tools

High-risk gateways often structure:

- Rolling reserves

- Volume caps

- Risk monitoring systems

These help manage exposure while allowing merchants to operate smoothly.

- Fast & Flexible Onboarding

Unlike traditional banks, high-risk gateways offer:

- Faster underwriting

- Industry-specific compliance support

- Dedicated account managers

- Robust Reporting & Analytics

Real-time dashboards provide insights on:

- Approval rates

- Fraud patterns

- Chargebacks

- Revenue trends

Comparisons of High-Risk Payment Gateways

| Feature / Option | High-Risk Payment Gateways (Specialized) | Offshore Merchant Processing | Onshore High-Risk Processors | Alternative Payment Methods |

| Definition | Payment gateways designed specifically for high-risk businesses | Payment processing through foreign banks/providers | Domestic processors that accept high-risk merchants | Non-traditional payment options (crypto, e-wallets, etc.) |

| Risk Acceptance | High (designed for high-risk industries) | High (foreign jurisdictions tolerate elevated risk) | Moderate (varies by bank) | Depends on method (crypto = high, e-wallets = moderate) |

| Regulatory Complexity | Moderate to high | High (multiple jurisdictions) | Lower (local rules, but strict) | Low to moderate (varies by method) |

| Approval Difficulty | Moderate | Lower than domestic | Higher than offshore | Often easy (especially crypto/e-wallets) |

| Processing Fees | Higher than standard gateways | High (includes offshore fees) | High | Low to moderate |

| Chargeback Handling | Specialized tools and support | Responsibility of provider | Standard but stricter | Varies (crypto = no chargebacks) |

| Settlement Speed | Standard to slow | Can be slower | Standard | Fast (crypto/e-wallets) |

| Compliance Requirements | PCI DSS, KYC, AML | International compliance + local laws | PCI DSS, KYC, AML | Minimal (varies by method) |

| Currency Support | Multi-currency | Multi-currency | Often limited | Crypto (global), e-wallets (varies) |

| Best For | High-risk industries needing reliable payment acceptance | High-risk businesses with rejected domestic applications | Businesses with borderline risk that can qualify locally | Startups, global micro-transactions, and users avoiding traditional banking |

| Examples | Specialized high-risk gateways | Offshore processing partners | Onshore banks with high-risk programs | • Cryptocurrencies • PayPal/Stripe (limited availability) |

| Pros | Built for high risk; fraud tools; industry support | Higher acceptance, multi-jurisdiction flexibility | Local banking familiarity | Easy setup; potentially lower cost |

| Cons | Higher fees; stricter requirements | Complex regulations; compliance overhead | Harder approvals | Limited integration; variable acceptance |

Comparison of High-Risk Payment Gateways (Countrywise)

| Region | Provider | Location / Coverage | Approx. Pricing | Reviews / Ratings | Resources |

| USA | PaymentCloud | USA focus, supports high-risk industries | ~$10–$45/month + 2.7–4.3% transaction fees; chargeback $25 | ~4.52/5 (strong integration & support) | https://www.paymentcloud.com/ |

| High Risk Pay | USA | ~$9.95/month + ~2.95% + $0.25 (varies) | ~4.5/5, high approval rate & easy setup | https://www.highriskpay.com/ | |

| Durango | USA | ~$45/month + ~2% | ~4.5/5, strong for highest-risk niches | https://durangomerchantservices.com/ | |

| National Processing | USA & international | ~$14.95/month + ~2.4% | ~4.8/5 value rating | https://nationalprocessing.com/ | |

| UK | PayPal (High-Risk Accounts) | UK & global | No fixed monthly; transaction fees vary (interchange + markup) | Trusted brand but complex fees | https://www.paypal.com/uk/ |

| WorldPay | UK & global | ~£19–£45/month + ~1.3–1.5% per txn (varies) | Well-known but long contracts | https://www.worldpay.com/uk | |

| ccNetPay | UK / EU | Annual fee ~€950 + per txn (~€0.15–€0.25) | Focuses on EU high-risk sectors | https://ccnetpay.com/ | |

| Merchant Connect | UK & Europe | Custom pricing | Strong fraud tools, GBP/EUR support | https://merchantconnect.uk/ | |

| Europe | WebPays | EU & global | Custom pricing (quote-based) | Good security & fraud protection | https://webpays.com/ |

| MoneyEU | Europe focus | ~$50–$200/mo + 2.5–5% per txn; rolling reserves common | ~4.4/5 Trustpilot (regional reviews) | https://moneyeu.com/ | |

| FastoPayments | US/UK/EU coverage | ~3%+ per txn (varies) | ~90% approval for high-risk merchants | https://fasto.co/ | |

| Instabill / iPayTotal | EU & global | Quote-based, multi-currency | Known for multi-currency & niche support | N/A |

Types of High-Risk Payment Gateways

Since having a good payment gateway is essential, knowing the pros and cons of each type will help you choose.

Redirection

The most direct payment experience, redirection, is best for new and small businesses as they are secure and easy to set up. Sellers dIn addition, sellers need to create a seller.

This gateway will redirect your customer to another payment page and effect the payment. In the meantime, you have an opportunity to advertise your brand at the checkout point by showing your logo. When using third-party redirect gateways, you can rely on them to provide the heavy lifting, be it the security protocols or even privacy requirements.

Yet, this may also be challenging, as you will not have such control over the process. The other disadvantage is that this approach would disrupt the shopping experience of the user. The consumer will be required to move out of the e-commerce site to make the online payment.

Buy on-site, pay off-site.

The purchase order process is complete on the site without any redirection, which speeds up the user experience.

However, this gateway will take customers off the site to complete a transaction. It implies that the sellers are left to provide security themselves. Your site has to be PCI compliant in order to safeguard consumer data and this takes additional resources and technical skills.

Order and Payment on the Site

This payment is ideal for large e-commerce companies hoping to generate a high sales volume. Everything will work through the seller’s system, from purchase to payment processing.

A third-party gateway will temporarily redirect your customer away from the site for the transaction. However, they won’t notice it as the hosted checkout page looks just like your eCommerce website.

This process can be supplemented by special offers or use of add-ons to influence people to purchase more items. The system will automatically send the users to your site after the transaction has been made. In that way, the customers will be able to continue browsing through the product pages and therefore this gives you more chances of securing conversions.

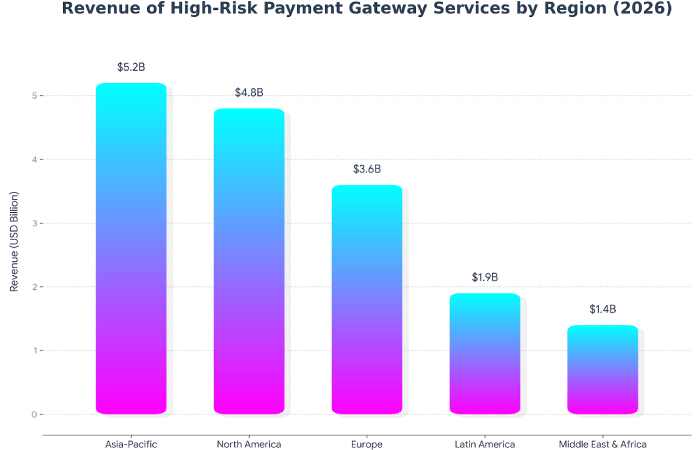

Revenue Of High-Risk Payment Gateway Services By Region

How does a High-Risk Payment Gateway Work?

There are four key players in every online deal: the buyer and the merchant, the issuing bank (which has issued the customer’s card), and the acquiring bank (which collects the funds from the issuing bank).

Although there are many steps, digital transactions usually take minutes.

Once the customer is ready to counter, the website will straight them to a payment gateway to enter credit card info or bank details.

The next step is encoding. After that, the payment gateway will encrypt the sensitive data between the buyer and the seller.

In addition, the gateway will perform fraud checks with built-in security protocols, such as TLS (Transport Layer Security).

After ensuring a secure connection, the issuing bank will check if there is enough equilibrium in the account.

If the seller’s account declines the transaction, the seller will ask the customer to choose another payment method. Some of the factors influencing approval are network errors, the seller’s maximum transaction limit, and bank-related issues.

What are the Top 5 Best Payment Gateways?

| Payment Gateway | Typical Pricing (Online) | Setup / Monthly Fees | Best For | Resource |

| Stripe | ~2.9% + $0.30 per transaction | No setup / no monthly fee | Scalable eCommerce & developers | Cotocus / scmGalaxy / LitExtension |

| PayPal | ~3.49% + $0.49 per transaction | No setup / no monthly fee | Trusted global gateway | LitExtension / Cotocus |

| Square | ~2.6% + $0.10 (U.S.) / ~2.9% + $0.30 online | No setup / no monthly fee | SMBs with online + in-store sales | Cotocus / scmGalaxy |

| Adyen | Variable pricing: ~€0.11 + method fee | None (custom quote) | Large enterprises & global brands | LitExtension / Cotocus |

| 2Checkout (Verifone) | ~3.5% + $0.35 per transaction | No setup / no monthly fee | Cross-border digital sales | LitExtension / scmGalaxy |

Examples of the Best Payment Gateways Existing for E-Commerce Businesses

| Payment Gateway | Pricing / Fees | Key Features | Best For | Resources |

| Stripe | ~2.9% + $0.30 per transaction (no setup/monthly fee) | Great APIs, subscriptions, global multi-currency, modern dashboard | Developers, global eCommerce | https://stripe.com/pricing |

| PayPal | ~2.9% + $0.30–$0.49 (varies by account type & region) | Widely trusted, buyer protection, supports wallet checkout | International stores, broad audiences | https://www.paypal.com/ |

| Authorize.Net | ~2.9% + $0.30 per transaction + ~$25/month gateway fee | Virtual terminal, recurring billing, fraud tools | Established retailers needing full gateway | https://www.authorize.net/ |

| Square Payments | ~2.9% + $0.30 per online transaction | Unified POS & ecommerce, inventory management | Omnichannel sellers & retail | https://squareup.com/ |

| Braintree (PayPal) | ~2.9% + $0.30 per transaction | Global support, PayPal + cards, seamless checkout | High-volume global eCommerce | https://www.braintreepayments.com/ |

| 2Checkout (Verifone) | ~2.59% + $0.49 per transaction | Global payments, multiple currencies | Cross-border digital product sellers | https://www.2checkout.com/ |

| Razorpay (India) | ~2% + GST (cards/UPI) & higher for international cards | UPI, wallets, subscriptions, fast onboarding | Indian eCommerce & SMEs | https://razorpay.com/ |

| PayU (India) | ~2% + GST domestically, ~3% + GST international | Local methods, analytics, fraud prevention | Indian merchants & small businesses | https://www.payu.in/ |

| Cashfree (India) | ~1.9% + GST (cards), ~0.4% UPI (varies) | Low fees, bulk payouts, API integrations | Indian ecommerce & payouts | https://www.cashfree.com/ |

| CCAvenue (India) | ~2% + GST domestic, ~3–4% international | 200+ payment options, multi-currency | Enterprises & multi-option checkout | https://www.ccavenue.com/ |

| Paytm (India) | Fees vary by method, UPI & wallet support | Instant settlement, robust local coverage | Mobile-first Indian shoppers | https://business.paytm.com/ |

Offshore Merchant Processing

| Aspect | Description |

| Definition | Offshore merchant processing is the use of payment gateways and merchant accounts based outside a business’s home country to process customer payments. |

| Target Businesses | High-risk businesses such as online gaming, forex, crypto, adult services, CBD, nutraceuticals, and subscription-based models. |

| Reason for Use | Domestic (onshore) banks often reject high-risk merchants due to chargeback risk, regulatory concerns, or fraud exposure. |

| Role in High-Risk Payment Gateways | Offshore processors specialize in supporting high-risk payment gateways with flexible underwriting and risk tolerance. |

| Payment Methods Supported | Credit cards, debit cards, international cards, recurring billing, and sometimes alternative payment methods. |

| Currency Support | Multi-currency processing allows merchants to accept payments from global customers. |

| Geographic Reach | Enables businesses to sell internationally without being limited by local banking regulations. |

| Approval Rate | Higher approval rates compared to onshore processors for high-risk merchants. |

| Fees & Costs | Generally higher than low-risk processing due to increased risk (higher transaction fees, rolling reserves). |

| Security Measures | Advanced fraud prevention, chargeback monitoring, encryption, and compliance tools. |

| Compliance Requirements | Must comply with international regulations, local laws, and card network rules (Visa, Mastercard). |

| Advantages | Access to global markets, higher acceptance rates, support for high-risk models. |

| Disadvantages | Higher processing fees, complex compliance, longer settlement times in some cases. |

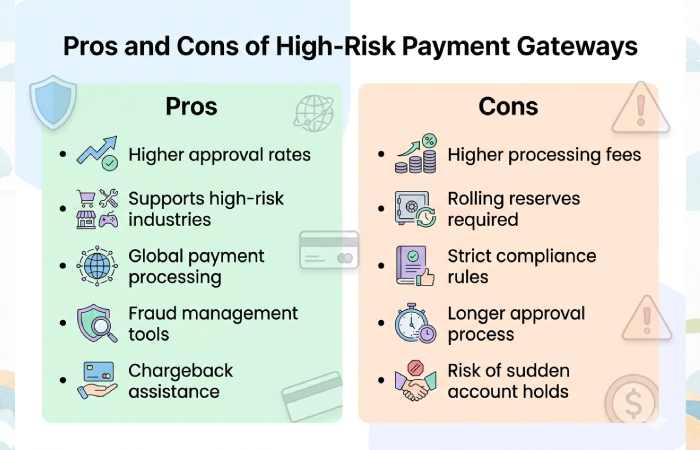

Pros And Cons Of High-Risk Payment Gateways

{kind=link}

Conclusion

Having a High-Risk Payment Gateway that guarantees the security of transactions and offers different payment methods (credit card, online banking, deferred or instalment payment, etc.) gives consumers confidence, improving their shopping experience and loyalty.